What is GST Return Filing?

Taxable persons and entities under GST are required to file various GST returns. Under GST, return filing is a very important activity that serves as the link between the taxpayer and the government. In the GST return, the taxpayer is required to furnish details like the particulars of business activity, declaration of tax liability, GST payment and other information as requested by the government. GST return filing electronically and facility is to be provided for manual filing of GST returns, wherein the return can be prepared offline and uploaded on the GSTN by the taxpayer or a facilitation centre.

Who should file GST returns?

Registered persons who are taxable under GST are required to file GST returns. Therefore, any registered person who has obtained GST registration but has not crossed the exemption limit (i.e., Rs.20 lakhs across India, except for Northeastern and Hill states wherein its Rs.10 lakhs) will not be required to file GST return until they cross the exemption limit. However, once the exemption limit is crossed and the taxpayer begins filing GST returns, even if there is no taxable supplied made or received during a period, the taxpayer is required to file a NIL return. Hence, not filing GST return is not an option and without filing the return of a period, next return cannot be filed.

Need help with GST?

Talk to an R K Associates GST Expert for help with GST registration, GST filing and more.

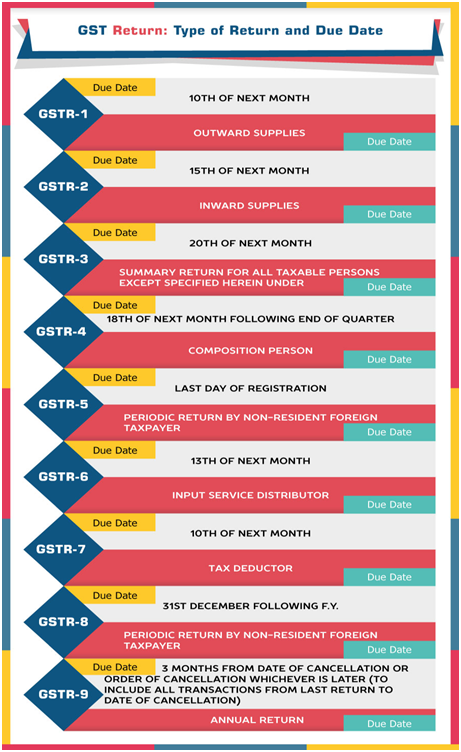

GSTR 1 Return of Outward Supply

GSTR-1 or return of outward supply must be filed by GST registered taxpayers before the 10th of every month. In the GSTR-1 or return of outward supply details like item wise detail of goods and services supplied with HSN or SAC codes, supply with respect to all B2B transactions, details of all inter-state supplies of B2C transactions above Rs.2.5 lakhs and all other invoices of less than Rs.2.50 lakhs with state wise summary details of all B2C transactions must be submitted. GSTR-1 should also contain details like zero-rated supplies, return of goods received in pursuance of an inward supply, exports, debit notes, credit notes and supplementary invoices.

GSTR 2 Return of Inward Supply

GSTR-2 or return of inward supply must be filed by GST registered taxpayers before the 15th of every month. In the GSTR-2 or return of inward supply, taxpayers are required to verify, modify or provide details of all supplied received during the period. Since, details of all inward supplies would have been filed by all taxpayers on the 10th of each month, most details in GSTR-2 would be auto-populated by the system. In addition, taxpayers are also required to declare details of all tax to be paid on reverse charge basis, import of goods or services, debit and credit notes and supplies received from persons not registered under GST and composition suppliers.

GSTR 4 Composition Scheme

GSTR-4 is a GST Return that has to be filed by a Composition Dealer. Unlike a normal taxpayer who needs to furnish 3 monthly returns, a dealer opting for the composition scheme is required to furnish only 1 return which is GSTR-4. It has to be filed on a quarterly basis.The due date for filing GSTR 4 is 18th of the month after the end of the quarter.GSTR-4 cannot be revised after filing on the GSTN Portal. Any mistake in the return can be revised in the next month’s return only. It means that, if a mistake is made in the GSTR-4 filed for the July-September quarter, the rectification for the same can be made only when filing the next quarter’s GSTR-4.

GSTR 3B

STR-3B is a monthly self-declaration that has to be filed a registered dealer from July 2017 till March 2018. Points to Note:

Ø You must file a separate GSTR-3B for each GSTIN you have

Ø Tax liability of GSTR-3B must be paid by the last date of filing GSTR-3Bfor that month

Ø GSTR-3B cannot be revised - Every person who has registered for GST must file the return GSTR-3B including nill returns.

Ø However, the following registrants do not have to file GSTR-3B

Ø Input Service Distributors & Composition Dealers

Ø Suppliers of OIDAR

Ø Non-resident taxable person

GSTR 3 Monthly Return

GSTR-3 or monthly GST return must be filed by GST registered taxpayers before the 20th of every month. In the GSTR-3 or monthly GST return, taxpayers are required to verify, and provide details of inward/outward supplies, input tax credit availed, tax payable, tax paid and other details as required. Majority of the information in the monthly GST return would be auto populated from the GSTR-1 and GSTR-2 return filed by the taxpayer on the 10th and 15th of each month. Only details to be provided by the taxpayer in GSTR-3 would be information relating to payment of tax and other information not previously provided in GSTR-1 and GSTR-2.

GSTR 9 Annual Return

GSTR-9 or annual GST return must be filed by GST registered taxpayers before the 31st December of the end of the financial year, in respect of which its filed. Annual GST return would be a detailed return which contains all the information filed by the taxpayer during the financial year, including income and expenditures under various heads, monthly tax payment reconciliation, refund details and pending arrears. In addition to the information submitted in the return, the taxpayer could also be required to furnish audited financial statements, reconciliation statements and other documents as required for the GST regulator from time to time.

Late Fees and Penalty

Interest is 18% per annum. It has to be calculated by the tax payer on the amount of outstanding tax to be paid. Time period will be from the next day of filing to the date of payment.

As per GST Act Late fee is Rs. 100 per day per Act. So it is 100 under CGST & 100 under SGST. Total will be Rs. 200/day. Maximum is Rs. 5,000. There is no late fee on IGST.

Late fees for GSTR-3B of July, Aug and Sept waived. Any late fees paid for these months will be credited back to Electronic Cash Ledger under ‘Tax’ and can be utilized to make GST payments.

As per Notification No. 73/2017 – Central Tax late Fee for filing GSTR-1, GSTR-3B and GSTR-4, GSTR-5, GSTR-5A and GSTR-6 after the due date have been reduced to:

Rs. 50 per day of delay

Rs. 20 per day of delay for taxpayers having Nil tax liability for the month.